By Forum Staff

While both the national and local economies have continued to grow moderately, with overall jobs and incomes rising, the growing burden of household debt is one troubling indicator, City Comptroller Brad Lander said on Tuesday as his Office released a special report on household debt across the five boroughs.

Household delinquency rates overall are still at relatively low levels—lower than before the pandemic—but they are up substantially from a year ago. In this Spotlight, we focus on trends in consumer debt, with the first published look at key trends in New York City.

There are five major categories of consumer debt: home mortgages, home equity lines of credit, student loans, auto loans, and credit cards. Delinquencies on mortgages have remained exceptionally low, primarily reflecting tighter underwriting since the 2008 recession, rising home values, and pre-pandemic low interest rates. Delinquency rates on student loans remain near zero at the moment, because the Department of Education has paused reporting on delinquent federal student loans (which comprise the majority of student loans) to credit bureaus until October 2024.

As a result, the two categories of consumer debt currently seeing high and rising delinquency rates are auto loans and credit cards. In this Spotlight, we focus on trends in household debt burdens and delinquencies for these two segments. To do this, Lander’s Office partnered with the Federal Reserve Bank of New York to focus on New York City specific credit data from the New York Fed’s Consumer Credit Panel, which is based on anonymized, individual credit report data from Equifax.

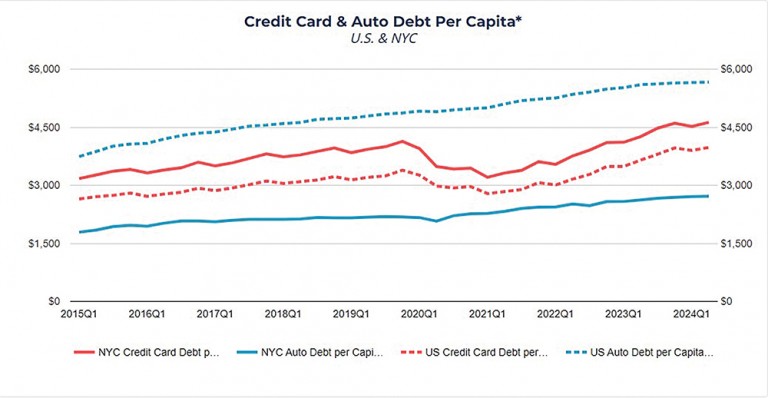

Nationwide, overall consumer debt levels have been growing slightly faster than income. Comparing the first half of this year with the first half of 2023, disposable income was up 3.8%, while total consumer debt was up 4 percent.

Nationally, 70 percent of consumer debt is in home mortgages. In contrast with the 2008 recession and its aftermath, most mortgage-holders today are in reasonably good shape because (1) mortgages have overwhelmingly gone to high credit score borrowers in the years since; (2) home values have risen so homeowners tend to have substantial equity in their homes; and (3) most of these mortgages are locked in at historically low interest rates from the years prior to the pandemic. As a result, mortgage debt has been rising more modestly in recent years, and delinquencies have remained low. Student loan debt has also been rising slowly, because accounts have not been accruing interest until recently, and new loan origination has been more subdued than pre-pandemic. Thus, most of the upward trend in debt and delinquency has been in auto and credit card debt, which are the focus here.

When the federal pandemic stimulus gave households a boost in 2020, debt levels and delinquency rates on credit cards declined, both nationally and in New York City. Credit card balances started to rise again in 2021. In contrast, auto loan balances maintained a fairly steady upward trend throughout. In the first half of 2024, auto loan balances among New York City residents were 6 percent above 2023 levels—a steeper rise than the nationwide increase of 3.2 percent. However, because vehicle ownership here tends to be well below average, this comprises a much smaller share of total debt locally (4 percent) than nationally (9 percent). Credit card debt, in contrast, represents an above-average share of total debt here, and it has been expanding rapidly so far this year—up 11 percent year-to-date over the first half of 2023, which is nearly triple the estimated growth in wage and salary income over the same period. Still, it should be noted that many consumers—both in New York City and nationally—paid down credit card debt during the pandemic and that the level of credit card debt appears to be roughly back on its pre-pandemic trend. In fact, both credit card debt and wage & salary income are up by an estimated 23 percent from 2019 levels.

Still, does this mean that a growing number of consumers are struggling financially? Or, are consumers simply using debt as a tool to spend more, consistent with rising incomes? Rising delinquencies suggest that distress may be on the rise among some consumers. Delinquency rates on both auto loans and especially credit cards have increased substantially over the past year. As of the second quarter of 2024, 12.2 percent of New Yorkers with credit card accounts were more than 90 days delinquent on at least one of them—up from 10.6 percent a year earlier and up from 10.1 percent at the onset of the pandemic. On auto loans, the share was not quite as high, at 8.4 percent —up from 7.5 percent a year earlier but down from 9.5 percent in the first quarter of 2020.

While debt levels and delinquency rates are useful metrics for gauging the debt burden on consumers, the rate at which debts become delinquent provides a more dynamic window into the financial stress of consumers. For both credit cards and auto loans, these new flows into delinquency now exceed pre-pandemic levels. Over the past year, while new delinquencies on auto loans (less pervasive in New York City than in the rest of the country, given lower rates of vehicle ownership) appear to have leveled off, newly delinquent credit card debt continued to climb, though the pace appears to have slowed in the 2nd quarter, both nationally and locally. The share of credit card debt in New York City that is newly delinquent, which was generally below 2 percent in the years before the pandemic, and which fell to as low as 0.6 percent in 2021, is now above 2.5 percent.

Residents of the Bronx appear to be facing the most financial stress, as new delinquencies are much higher than in the rest of the city and still appear to be rising. In contrast, Manhattan households have consistently seen the lowest flows into delinquency and they have leveled off. In the middle of the pack are Queens and Brooklyn, while Staten Island is somewhat below (i.e. better off than) the city-wide average. One likely driver of this is that the Bronx has the highest poverty rate and that lower income consumers tend to face greater financial stress than more affluent households. Bronx residents saw the biggest drop following the application of federal pandemic stimulus, with the share of newly-delinquent credit card debt falling from over 3 percent in 2019 to below 1 percent in 2021. This is consistent with a January 2023 report showing that Bronx resident benefitted significantly from federal pandemic stimulus. Unfortunately, the share of newly-delinquent credit card debt has now risen to nearly 4 percent.

In the Consumer Credit Panel, income data are not available for individuals. However, it is possible to get a rough idea of how various income groups are faring by looking at the zip code of residence. Specifically, the comptroller looks at trends across four groups (income quartiles) of zip codes based on the average adjusted gross income in each zip code (derived from 2020 IRS statistics of Income), which we place into four, equal population size groups: high income, moderately high income, moderately low income, and low income.

While the overall level of credit card debt has been climbing citywide since 2021, growing debt burdens have hit the city’s poorest neighborhoods particularly hard. Since the end of 2019, debt levels are up just 8 percent in the more affluent neighborhoods (i.e. “high income” zip codes shown in the map above), while they are up 24 percent in the lowest-income neighborhoods.